Getting a Shared Ownership Mortgage With Bad Credit

See how a specialist broker can help you if you're looking for a shared ownership mortgage but you have bad credit

Firstly, are you looking to purchase a shared ownership / shared equity property?

Why use us?

At OnlineMortgageAdvisor we know that everyone's circumstances are different. That's why we only work with specialist brokers, who are experts in securing mortgage approvals.

-

Specialists in shared ownership mortgages

Specialists in shared ownership mortgages -

Higher chance of approval

-

We don't charge a fee

-

No impact on credit score

-

Mortgage Approval Guarantee - or £100 back*

-

Rated excellent on Trustpilot, Feefo and Google

If you have any questions,

feel free to call us on 0808 189 2301

Author: Pete Mugleston

Mortgage Advisor, MD

Criteria Brain

https://mortgagebrain.com/products/criteria-brain/We’ll explain how bad credit could affect your chances of securing a Shared Ownership mortgage, what you can do to strengthen your application and why speaking to a specialist broker will ensure you don’t apply blindly and end up causing more damage to your credit files.

In this article:

What is shared ownership?

Shared ownership is a unique government-supported scheme that offers a more affordable way for people to buy a property without needing a significant deposit.

As the name suggests, it allows you to buy a share of a property rather than all at once and you can gradually increase the amount you own during the mortgage term.

How are shared ownership mortgages different?

For a standard mortgage, you would need a deposit and then a mortgage for the remaining balance. With shared ownership you purchase a pre-agreed portion of a property using a mortgage – typically between 25% and 75% – and pay rent on the remaining amount to a local housing association.

You can increase the ‘share’ you own in the property during the mortgage term – this is known as ‘staircasing’ – so, eventually you can own all of the property once all the mortgage debt has been repaid.

Typically aimed at first-time buyers, this is a great way to get on the property ladder if you’re struggling to raise a large deposit because for shared ownership your deposit is calculated based on the percentage of the property you’re buying, rather than the full value.

Can you get a Shared Ownership mortgage with bad credit?

Yes. Shared Ownership is a government scheme that can help people who want to buy or move but are struggling to get together a big enough deposit and don’t mind the idea of co-owning their home.

As far as acceptance into the scheme is concerned, bad credit should not be a barrier. However, once you are accepted for a Shared Ownership property and need to get a mortgage, it can make things a little more complicated.

This is because adverse credit makes lenders wary that you may struggle to make the repayments which can restrict your borrowing options. But there are plenty of lenders out there willing to consider an application – even if you have some severe adverse on your credit files.

Speak to a Shared Ownership mortgage expert

Maximise your chance of approval with a dedicated specialist broker

How to get a Shared Ownership mortgage with bad credit

If you’re considering applying for a Shared Ownership mortgage but have poor credit, make an enquiry with us so we can match you with a specialist bad credit mortgage broker to boost your chances of approval and landing the best possible deal.

The broker we handpick for you will walk you through the following steps…

- Calculating your affordability to work out how much you can borrow and your monthly repayments based on the portion of the property you’re buying

- Downloading and optimising your credit reports to strengthen your application. Just click on the link above to start your free trial and download all your reports straight away.

- Finding the ideal mortgage lender, with the best available interest rates, for someone applying through the scheme with poor credit

- Advise you on the specific paperwork and requirements for a shared ownership application – such as registering with the local housing association where the property you’re looking to buy is located

How do credit issues affect shared ownership mortgages?

Different types of credit issues will affect your shared ownership application in varying ways. Some may not affect it at all whereas others could result in an instant rejection as explained in more detail below.

Not severe

The following credit issues are unlikely to result in your application being out and out declined as long as you can present an acceptable explanation as to why they have occurred and the steps you’ve taken to improve your credit record:

- Late payments

- Low credit score

- No credit history

Severe

These types of credit issues may affect your chances of success with certain mortgage lenders but others could be willing to still consider your application depending on the time since they occurred and the amounts involved:

- County Court Judgement (CCJ)

- Missed mortgage payments

- Defaults

- Payday Loans

- IVAs

- Debt Management Plans

Very severe

These credit issues will be the most challenging to overcome and will most likely result in your application being declined by most mortgage lenders if they’re still showing on your credit record at the time:

- Bankruptcy

- Repossession

- Multiple credit problems

Regardless of the type of credit issue you’ve suffered, the smart move is to first approach a mortgage broker with experience arranging mortgages for people with bad credit rather than applying directly to a lender.

They will be able to identify specialist lenders who have a track record of helping people secure shared ownership mortgages who have had similar credit issues.

Deposit requirements

Typically, a deposit of at least 5% is needed to get a mortgage through this scheme. However, if you also have a bad credit record then, depending on the severity of the issue (as outlined above), you may well need a higher deposit – typically between 15%-20% – to give yourself a better chance of getting approved. The higher your deposit will also mean more mortgage lenders willing to consider your application.

It may be possible to get a 100% Shared Ownership mortgage, but, realistically, not with bad credit on your record.

Other eligibility factors

Affordability is a major factor in a lender’s decision as they are legally obliged to check you can make the repayments. They do this by examining your income and expenses so most experts would suggest that you, ideally, ditch any unnecessary subscriptions at least three months before applying.

Fortunately, bad credit mortgage lenders tend to have a flexible approach to underwriting. So, if your credit history is holding you back but affordability is ok, it’s worth speaking to a bad credit mortgage broker to discuss your options.

Other criteria to think about are:

- Age – Most lenders have an upper age limit for borrowers. This might mean you could face rejection with some, not because of your bad credit per se, but because the shorter borrowing period and higher rates make a loan unaffordable.

- Property type – Rarely an issue with Shared Ownership properties, but it’s worth keeping in mind that some providers won’t lend on anything other than a standard construction bricks and mortar home.

- Staircasing – This refers to the practice of increasing the amount of the property you own over time. Some lenders will not approve a mortgage if there are restrictions on how much of the property you can buy – so check the terms and conditions carefully.

- Loan to value – For Shared Ownership, this refers to the value of your share of the property. Lenders may set a maximum LTV for this type of property or for anyone with more severe credit issues such as CCJs or bankruptcy.

We're so confident in our service, we guarantee it.

We know it's important for you to have complete confidence in our service, and trust that you're getting the best chance of mortgage approval at the best available rate. We guarantee to get your mortgage approved where others can't - or we'll give you £100*

How you can improve your chances of being accepted with bad credit

There are a number of steps you can take to boost your chances of success, despite your poor credit record. These include:

- Review your credit reports to check for any inaccuracies – it’s really important to make sure your credit records are completely up to date. If there’s any information that can be removed you can do that before submitting your application

- Saving up for a higher deposit – shared ownership schemes may not need as much deposit as for standard mortgages, however, the more you save, the more lenders will consider your application as this lessens the risk involved with your bad credit issues

- Make a joint application – if you have a partner (or a close family member) who has a stronger credit record then applying for a joint mortgage would represent a more solid case for being accepted by a mortgage lender

- Using the services of a mortgage broker – they can use their extensive knowledge and experience in this area to help you optimise your credit records and identify the right lenders who have a history of accepting shared ownership mortgage applications from someone who has bad credit.

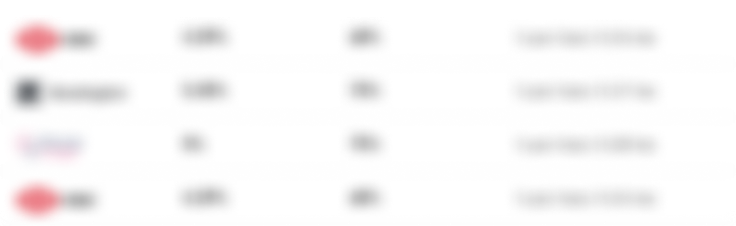

Typical interest rates

Interest rates for bad credit mortgages are no different if you are applying through the Shared Ownership scheme. Take a look at our rates table below to get an idea of the current deals available, but please note that the rates are subject to change.

Looking for more rates and deals?

We can match you with a mortgage broker who can provide you with up-to-date bespoke rates and deals from across the entire market.

Last updated July 2024

The rates quoted above were correct at the time of writing and are subject to change at any time at the lender’s discretion. Speaking to a mortgage broker is the best way to keep track of the rates available at any given time.

Which lenders offer this type of mortgage?

Several mainstream lenders will consider poor credit mortgages for Shared Ownership depending on the severity of the issues, when they occurred and whether they are now sorted.

For example, Barclays, Halifax and Santander may consider an application if you have a few late payments on your credit card, but not if you have a recent CCJ.

The more severe and recent your credit problems, the more likely you are to need a specialist lender.

Alternative options for bad credit borrowers

If you feel the shared ownership scheme isn’t the right option for you or you’ve been unable to secure the mortgage you need then don’t be despondent! There are still other alternatives you can consider, such as:

- A guarantor mortgage – otherwise known as a family-assisted mortgage

- Other Government mortgage schemes – such as the First Home Scheme (aimed at first-time buyers) or Right To Buy

- Gifted deposits – a higher deposit, gifted by a family member, for example, could make all the difference between your mortgage application being successful or not

- A joint borrower sole proprietor mortgage – also known as joint mortgage single ownership mortgages

Superb response and knowledgeable advisor

Steve, the financial advisor, contacted me within the hour and was very friendly, knowledgeable and professional. He seemed to relish my non standard requirement, diligently kept me updated during the day and we struck up a great relationship. Very impressed.

Peter Costello

Knowledgeable and Supportive

The team were fantastic and really knowledgeable and supportive. They answered all questions promptly and came back to me with regular updates. I have already recommended them and will use them again.

Dorothy

Prompt and Professional

A very prompt and professional service. The advise and guidance has been so valuable as a first time buyer.

Ayesha

Rated 4.8 out of 5 stars across Trustpilot, Feefo and Google

Get matched with a Shared Ownership mortgage broker who specialises in bad credit

Bad credit and Shared Ownership mortgages are common bedfellows, and you shouldn’t let your adverse deter you from applying. But it’s important to get the right advice the first time as rejected applications can cause further harm to your credit files.

We work with brokers who have deep knowledge of the bad credit mortgage market and solid working relationships with lenders who specialise in the scheme. They will assess your individual circumstances before narrowing down your options to the most suitable lenders for you.

They can also act as an advocate to help get a deal over the line in some circumstances.

Our broker matching service will pair you up with the most appropriate broker based on your situation. To get matched with your ideal broker call 0808 189 2301 today or enquire online.

Speak to a Shared Ownership mortgage expert

Maximise your chance of approval with a dedicated specialist broker

FAQs

There is no single, universal credit score and some lenders do not apply credit scoring to applications at all. But if you have poor credit, it’s often best to speak to a specialist lender who assesses applications on a case-by-case basis rather than by applying a numerical score.

Yes, all mortgage lenders will conduct credit checks as part of their wider eligibility criteria requirements. This allows them to thoroughly consider all aspects of your application and not just your credit history.

So, for example, if someone has a less severe credit issue such as some late payments but they also have a high amount of disposable income and a large deposit then they may view the overall application as being strong enough to be accepted.

It’s possible, but as outlined above, a CCJ is considered a severe form of bad credit. It will depend on the amount involved and the time since the CCJ was resolved.

It’s also really important you choose the right lender who has experience accepting shared ownership mortgage applications for people with CCJs. This is where a mortgage broker can help – they will know who these lenders are and can identify them for you.

About the author

Pete, an expert in all things mortgages, cut his teeth right in the middle of the credit crunch. With plenty of people needing help and few mortgage providers lending, Pete found great success in going the extra mile to find mortgages for people whom many others considered lost causes. The experience he gained, coupled with his love of helping people reach their goals, led him to establish Online Mortgage Advisor, with one clear vision – to help as many customers as possible get the right advice, regardless of need or background.

Pete’s presence in the industry as the ‘go-to’ for specialist finance continues to grow, and he is regularly cited in and writes for both local and national press, as well as trade publications, with a regular column in Mortgage Introducer and being the exclusive mortgage expert for LOVEMoney. Pete also writes for Online Mortgage Advisor of course!

Pete Mugleston

Mortgage Advisor, MD